Every nonprofit today depends on digital convenience to drive donor participation. Yet beneath the surface of every contribution lies a crucial financial decision — which payment method to prioritize. Between ACH payments, card payments, and digital wallets, each channel carries its own balance of cost, speed, and donor experience. Understanding these trade-offs is essential for organizations that rely on online giving as their primary source of support.

While innovation in payment methods for nonprofits has made it easier than ever to accept online transactions, every choice directly affects conversion rates, processing fees, and overall donor satisfaction. What may work for an e-commerce store might not align with the needs of a mission-driven organization that values recurring support and predictable cash flow. The goal, therefore, is not just to adopt new technology but to match the right payment method with the right giving behavior — ensuring both donors and finance teams benefit equally.

Understanding ACH Payments and How They Work

ACH payments (Automated Clearing House transfers) move funds directly between bank accounts without relying on card networks. For nonprofits, this method offers lower payment processing fees and stable recurring revenue for supporters who prefer long-term engagement. ACH operates as a batch-based system where transactions are collected, verified, and processed within one to two business days. This slightly slower speed compared to instant card payments is offset by significant savings, particularly for large donations or monthly giving programs.

For nonprofits seeking to maximize the impact of every dollar, ACH becomes a powerful tool. Processing costs typically range from 0.5% to 1%, compared to 2.5–3% for card payments. Donors also appreciate the reliability — once authorization is granted, recurring deductions happen automatically, requiring minimal intervention. When integrated into payment methods for nonprofits, ACH simplifies reconciliation and reduces chargeback risks. For campaigns focused on sustainability rather than speed, this channel offers unmatched efficiency.

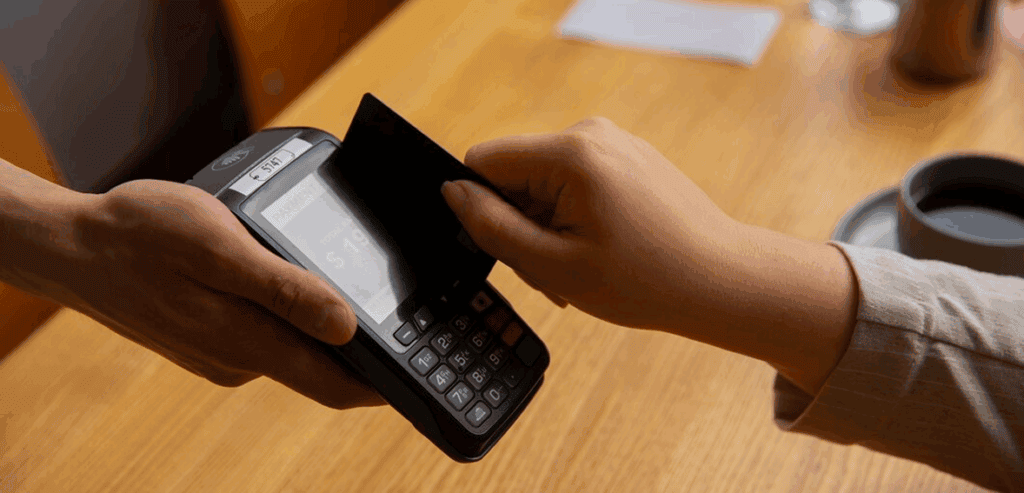

The Ubiquity and Flexibility of Card Payments

Credit and debit card payments dominate the landscape of online transactions. They are instant, universally recognized, and easy for donors to use on any device. For nonprofits, card processing provides a predictable and familiar checkout experience that can boost immediate donor conversion rates. However, this convenience comes at a cost. Transaction fees typically hover between 2.9% and 3.5%, depending on the processor and card type.

Despite the higher cost, card payments remain vital because of their accessibility. A donor halfway across the world can contribute in seconds using a Visa or Mastercard. When integrated within a modern giving platform, card-based recurring donations are easy to manage and adjust. Many organizations absorb the higher fees in exchange for frictionless engagement and faster deposits. Especially during urgent fundraising events or one-time campaigns, credit and debit cards are often the best option to drive immediate participation and emotional response.

Digital Wallets: The Future of Frictionless Giving

Digital wallets such as Apple Pay, Google Pay, and PayPal have redefined online transactions by minimizing steps between intent and completion. For nonprofits, adopting wallets means aligning with modern donor behavior. Younger supporters and mobile-first contributors increasingly expect tap-to-donate convenience. By offering wallet options at checkout, nonprofits can dramatically improve donor conversion rates, particularly on smartphones.

The speed of digital wallets makes them ideal for time-sensitive campaigns or peer-to-peer fundraising. Donors no longer need to type card numbers or account details; biometric authentication completes the process securely. Wallet providers handle encryption and tokenization, ensuring strong compliance without additional integration complexity. While payment processing fees are similar to or slightly higher than cards, conversion improvements often justify the added cost. In campaigns driven by convenience, wallets serve as both a payment tool and a trust signal.

Comparing Costs Across Payment Methods

When analyzing cost structures, nonprofits must look beyond surface fees. While ACH payments clearly offer the lowest transaction cost, they may involve delayed settlement and limited international reach. Card payments incur higher payment processing fees, but they deliver faster deposits and wider acceptance. Digital wallets, on the other hand, combine the instant nature of cards with mobile convenience, though at the upper end of the cost spectrum.

The right balance depends on the organization’s donation mix. A nonprofit that handles numerous small donations from global supporters may favor cards or wallets for speed and familiarity. In contrast, those with predictable monthly pledges benefit more from ACH payments, which keep overhead minimal and retention strong. Cost optimization comes from offering donors multiple choices while steering them subtly toward the most sustainable options.

Conversion and Donor Behavior Insights

Beyond fees, donor psychology determines the real value of a payment method. Research consistently shows that reducing friction at checkout improves donor conversion rates. Donors are more likely to complete online transactions when their preferred method is available. If a giving form supports cards, digital wallets, and ACH payments, it removes hesitation and builds trust.

For recurring donations, ACH and saved card profiles excel due to automation. The fewer steps required to give again, the higher the likelihood of continued support. Wallet payments, particularly on mobile devices, also see high repeat usage because they eliminate the need for re-entering information. Nonprofits that analyze donor data through CRM integrations can identify which methods correlate with higher lifetime giving and tailor future campaigns accordingly.

The Role of Recurring Donations in Payment Selection

Recurring donations are the financial heartbeat of a nonprofit. They stabilize revenue and allow better forecasting. ACH-based recurring giving offers minimal cost per transaction, making it the preferred choice for long-term donors. However, card payments and digital wallets provide better accessibility for first-time contributors who may later transition to ACH once trust is built.

A blended approach works best. Use card payments and digital wallets for initial conversion and event-driven campaigns, then invite donors to switch to ACH for sustainability. By aligning cost-efficient methods with predictable revenue streams, nonprofits can protect margins while growing their donor base. This thoughtful segmentation ensures both short-term impact and long-term loyalty.

Trust and Security Considerations

Donors expect seamless and secure online transactions. Regardless of the payment method, data protection plays a decisive role in confidence. ACH payments use bank-grade encryption and pass through regulated financial networks, ensuring reliability. Card payments follow PCI DSS compliance, while digital wallets employ tokenization and biometric verification. Each channel meets global standards, yet user perception differs — wallets often feel more modern and private, while cards remain universally accepted.

For nonprofits, transparent communication about security can directly influence donor conversion. Displaying trust badges, secure connection symbols, and concise language about encryption reassures supporters. Whether using ACH or card-based systems, integrating a compliant payment gateway minimizes risk. When trust and technology move together, conversions rise naturally.

The Impact of Payment Processing Fees on Donations

Every percentage point in payment processing fees affects how much of a donation reaches the mission. Small differences compound quickly when multiplied by thousands of transactions. Nonprofits must evaluate total cost, including gateway fees, platform charges, and refund policies. ACH payments stand out for efficiency, often costing one-third of card processing. However, delayed settlement might affect cash flow in campaigns that require instant access to funds.

Digital wallets typically charge a flat fee similar to card processors but can reduce abandonment rates. The trade-off between cost and conversion is not always linear. For many organizations, slightly higher fees are acceptable if they translate into greater overall giving volume. Strategic planning means understanding both numbers — the cost of processing and the cost of lost opportunities when donors drop off mid-transaction.

Payment Methods for Nonprofits: Finding the Right Mix

A modern donation experience should accommodate diverse preferences. Offering ACH payments, card payments, and digital wallets together ensures inclusivity and flexibility. But nonprofits should still encourage efficient behavior. For high-value or recurring donors, ACH should be the default option. For quick, emotional campaigns or peer fundraising, digital wallets and card payments make the process spontaneous and familiar.

Technology platforms now allow nonprofits to customize these flows intelligently. Donation pages can suggest the lowest-fee method or allow recurring donors to switch channels easily. When properly managed, payment diversity enhances both user satisfaction and financial performance. The more a nonprofit aligns its payment methods for nonprofits strategy with donor habits, the stronger its overall sustainability becomes.

Enhancing Donor Conversion Through Checkout Design

Even with multiple payment options, poor design can hinder success. Donation forms should prioritize clarity, speed, and mobile responsiveness. Each additional click lowers donor conversion probability. Wallet icons should be visible, and ACH enrollment should be simple but secure. By reducing visual clutter and guiding donors smoothly through the process, nonprofits increase completion rates.

Modern giving software integrates all payment methods for nonprofits under a unified, PCI-compliant interface. This reduces donor confusion and operational friction simultaneously. Ultimately, conversion optimization is not just about adding payment options but refining how donors experience them — clean design, fast loading, and clear reassurance combine to build confidence and generosity.

International Donations and Currency Considerations

For organizations that receive online transactions from global supporters, card payments and digital wallets offer natural advantages. They support multi-currency processing, real-time exchange, and wide compatibility. ACH systems, being regional, primarily serve domestic donors. However, many platforms now include global equivalents like SEPA or EFT that extend the same low-cost principle internationally.

To maximize conversion abroad, nonprofits should enable at least one wallet option that handles cross-border payments seamlessly. Supporters outside the home country appreciate being able to donate without currency confusion. Transparency in exchange rates and fees also matters — clarity improves trust and encourages repeat giving. When paired with a compliant processor, international payments can be as simple and secure as domestic ones.

Speed, Settlement, and Operational Impact

Timing affects not just donors but internal teams. Card payments and digital wallets settle almost instantly, improving cash availability for urgent initiatives. ACH payments, though slightly slower, ensure predictability and reduce reversal risks. Finance departments must balance immediacy against dependability. For example, a campaign raising emergency relief funds might prioritize cards and wallets for speed, while long-term pledges rely on ACH for cost-effectiveness.

The operational benefit of faster settlement must be weighed against the accumulated fee expense. Many organizations adopt tiered strategies — defaulting to low-cost ACH for recurring donations while reserving faster methods for time-sensitive events. Such hybrid logic delivers both liquidity and savings, strengthening overall financial health.

Leveraging Data from Payment Analytics

Each payment method provides valuable insight into donor preferences. Analytics from ACH payments, card payments, and digital wallets can reveal trends in giving frequency, transaction size, and retention rates. For instance, recurring ACH donors might display higher lifetime value due to lower friction and fees. Meanwhile, wallet users may represent a younger, mobile-centric audience responding to social media appeals.

Integrating these insights into a nonprofit CRM allows teams to personalize outreach. Donors can be segmented by payment behavior, with targeted messages encouraging them to switch to the most efficient method. This data-driven approach transforms payment processing from a back-office function into a growth strategy, improving both engagement and efficiency.

Future Trends in Nonprofit Payment Systems

As digital ecosystems evolve, the boundaries between ACH payments, card payments, and digital wallets are blurring. Embedded finance, open banking, and instant transfer networks promise real-time movement of funds at minimal cost. For nonprofits, this shift will mean faster reconciliation, lower fees, and greater control over donor experience.

Wallets will continue expanding beyond convenience into community engagement tools, allowing direct integration with social platforms. ACH will likely modernize with same-day settlements, closing the gap with cards. The key for nonprofits is adaptability — choosing payment methods for nonprofits that evolve alongside donor expectations while keeping compliance and security intact.

Evaluating True ROI of Each Payment Method

Ultimately, the best payment method is the one that maximizes mission impact. ACH payments shine when recurring stability and cost savings are priorities. Card payments deliver instant results for campaigns needing rapid response. Digital wallets lead in mobile-first conversion and ease. Calculating ROI involves comparing net donation volume after fees against administrative simplicity and donor satisfaction.

When measured holistically, offering all three channels provides the most balanced outcome. Nonprofits that track metrics like conversion rate, donor lifetime value, and average transaction cost gain the clarity to optimize continuously. Technology, data, and compliance converge to ensure that every dollar given travels efficiently and securely to its purpose.

Conclusion

Choosing between ACH payments, card payments, and digital wallets is no longer a binary decision — it is a strategic exercise in aligning cost, convenience, and donor psychology. Each method plays a distinct role in shaping how effectively nonprofits manage online transactions and inspire generosity.

By combining cost-efficient ACH transfers, widely accepted card processing, and frictionless wallet experiences, organizations create donation journeys that feel both secure and effortless. The result is higher donor conversion, stronger recurring donations, and improved financial transparency. When nonprofits design their payment methods for nonprofits with this balance in mind, they not only process payments — they build lasting trust and sustained impact.